2027 is shaping up to be a key inflection point for US Warehouse Construction. While warehouse construction activity has remained subdued since the post-pandemic correction, a growing number of macroeconomic and industry indicators suggest the market is approaching the beginning of its next investment cycle. Industrial real estate fundamentals are improving as vacancy rates begin to stabilize and leasing activity strengthens. Meanwhile, industrial completions have fallen sharply, reducing future supply pressure, while stronger leasing volumes and improving occupier demand point to a more favorable environment for warehouse investment. At the same time, large occupiers across e-commerce, the grocery, automotive, semiconductors and data center logistics sectors have announced major new construction projects scheduled for completion from 2027 onwards. Together, these indicators suggest the industry is transitioning from a period of absorbing excess capacity toward the next phase of logistics infrastructure expansion.

2027 is shaping up to be a key inflection point for US Warehouse Construction. While warehouse construction activity has remained subdued since the post-pandemic correction, a growing number of macroeconomic and industry indicators suggest the market is approaching the beginning of its next investment cycle. Industrial real estate fundamentals are improving as vacancy rates begin to stabilize and leasing activity strengthens. Meanwhile, industrial completions have fallen sharply, reducing future supply pressure, while stronger leasing volumes and improving occupier demand point to a more favorable environment for warehouse investment. At the same time, large occupiers across e-commerce, the grocery, automotive, semiconductors and data center logistics sectors have announced major new construction projects scheduled for completion from 2027 onwards. Together, these indicators suggest the industry is transitioning from a period of absorbing excess capacity toward the next phase of logistics infrastructure expansion.

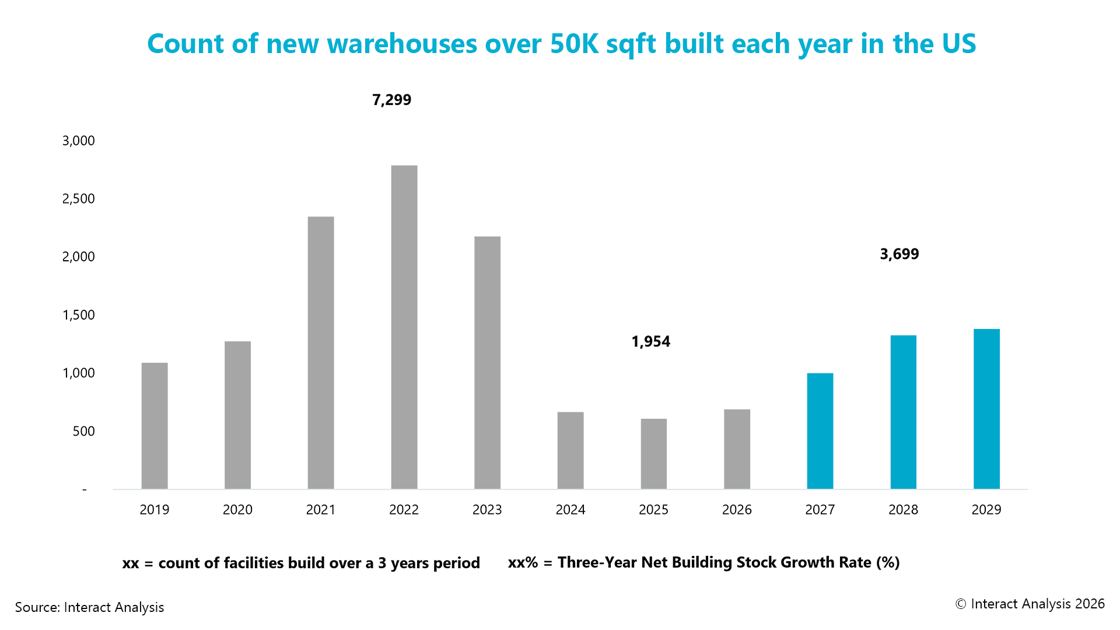

These improving market fundamentals are reflected in our Warehouse Building Stock Database and underpin our forecast that 2027 will mark the beginning of the next warehouse construction cycle. Following the sharp post-pandemic slowdown, annual net additions of large warehouses fell from more than 2,700 facilities in 2022 to fewer than 700 in both 2025 and 2026. As industrial supply and demand return to a more balanced position, we forecast activity to accelerate to almost 1,000 new facilities in 2027, before exceeding 1,300 facilities annually between 2028 and 2030. Looking beyond annual volatility, the underlying trend becomes even clearer. The rolling three-year total of new warehouse deliveries is forecast to increase from approximately 1,950 facilities during the 2024/26 period to around 3,700 facilities in the next investment cycle, an increase of 89%. While this remains below the exceptional levels seen during the pandemic-driven construction boom, it represents a meaningful recovery in greenfield warehouse investment and the start of a more sustainable period of long-term growth.

|

The Next Wave of Warehouse Construction Is Being Driven by Six Megatrends

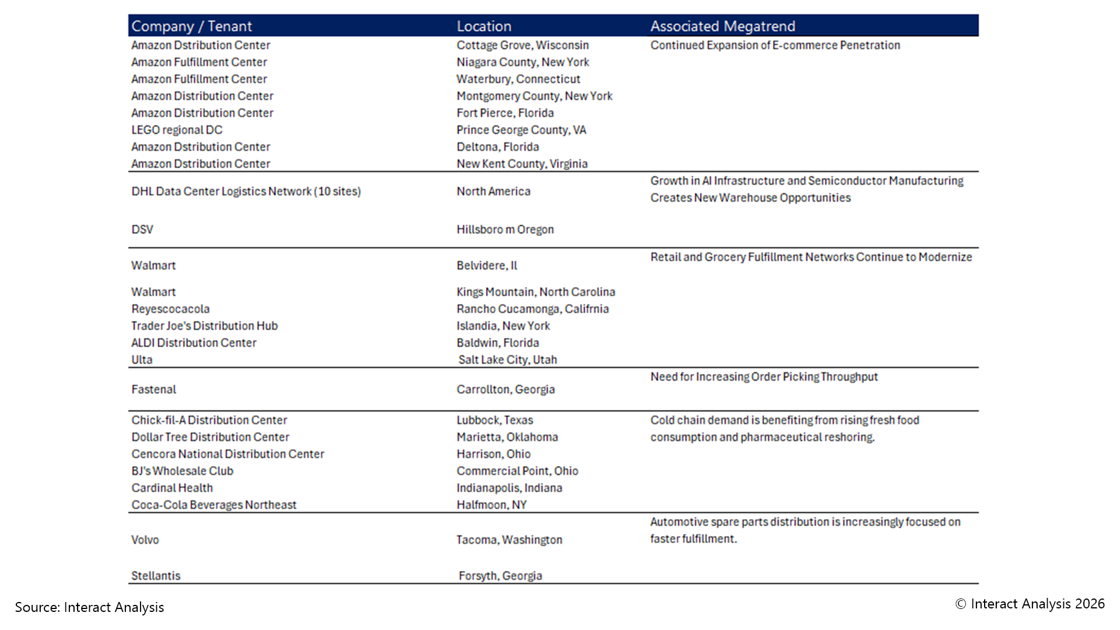

A sample of some of the largest warehouse projects currently under construction in the United States highlights six structural megatrends shaping the next investment cycle. The continued expansion of e-commerce remains the primary driver of warehouse construction, supporting investment in larger, higher-throughput, and increasingly automated fulfillment facilities. At the same time, retailers and grocers continue to modernize their distribution networks to improve efficiency and support omnichannel operations. Beyond traditional logistics, rapid growth in semiconductor manufacturing and AI data center infrastructure is creating demand for specialized logistics networks, while rising throughput requirements are encouraging further investment in warehouse automation. Meanwhile, cold chain demand is benefiting from stronger fresh food consumption and pharmaceutical reshoring, and automotive OEMs are increasingly prioritizing faster spare parts fulfilment. Together, these projects provide an early indication of where future warehouse investment opportunities are likely to emerge.

|

1) Continued Expansion of E-commerce Penetration

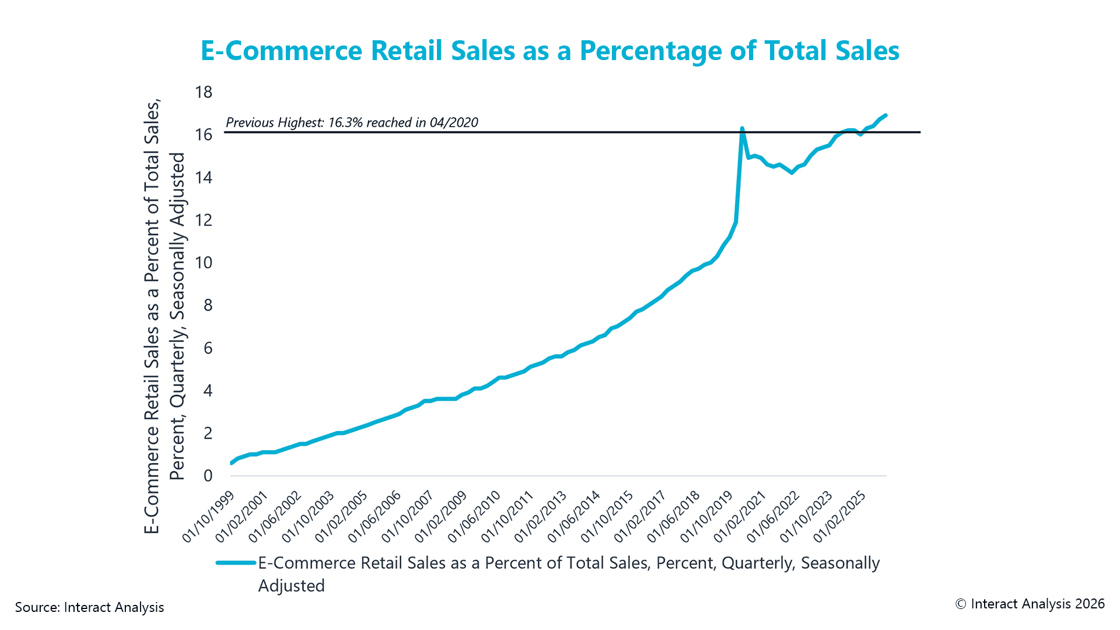

E-commerce penetration in the United States is higher than ever, surpassing even the peak reached during the Covid-19 pandemic when many physical stores were temporarily closed. This sustained shift in consumer behaviors remains a major driver of warehouse construction, as retailers and brands invest in larger and more automated fulfillment networks to support faster delivery and rising order volumes. Amazon alone is developing several facilities scheduled to come online in 2027, including large distribution centers in Wisconsin, Virginia, Florida, New York, and Connecticut, many of which will incorporate advanced robotics and support round-the-clock operations. At the same time, LEGO is investing more than $360 million in a 2 million-square-foot regional distribution center in Virginia to strengthen its North American supply chain and respond faster to changing demand. Together, these projects highlight how structurally higher e-commerce penetration is continuing to drive investment in high-capacity, technology-enabled logistics infrastructure.

|

2) Growth in AI Infrastructure and Semiconductor Manufacturing Creates New Warehouse Opportunities

Semiconductor and data center growth is emerging as a new source of demand for warehouse construction in the United States. The rapid expansion of hyperscale AI infrastructure and semiconductor manufacturing is creating increasingly complex supply chains that require specialized logistics capabilities and greater inventory capacity. Reflecting this trend, DHL is adding ten dedicated data center logistics sites across North America, totaling more than 7 million square feet, to support hyperscale data center deployments and provide services such as rack pre-configuration, white-glove handling, and specialized transportation. At the same time, DSV is constructing a new 750,000-square-foot regional hub in Hillsboro, Oregon, dedicated to serving semiconductor manufacturers. Together, these projects highlight how growth in AI, semiconductors, and data centers is creating new opportunities for logistics infrastructure investment and driving demand for specialized warehouse facilities.

3) Retail and Grocery Fulfilment Networks Continue to Modernize

Retail and grocery fulfillment networks continue to modernize as retailers invest in larger, more automated, and omnichannel distribution infrastructures. Rising e-commerce volumes, and growing expectations for faster delivery are driving a new wave of investment across the sector. Walmart is building highly automated facilities in Illinois and North Carolina to support grocery and large-item e-commerce fulfillment, while Ulta is adding an AutoStore-equipped distribution center in Utah to improve delivery speeds and support omnichannel operations. Grocery chains are also expanding their logistics footprints, with ALDI investing $9 billion through 2028, including new distribution centers and digital capabilities, and Trader Joe’s constructing a 921,000-square-foot facility on Long Island with dedicated cold and freezer storage.

4) Growing Demand for Faster Order Picking

The need for higher order picking throughput is increasingly driving warehouse investment as distributors seek faster fulfilment and improved product availability. Reflecting this trend, Fastenal is building a new regional logistics center in Carrollton, Georgia, with capacity to expand to 900,000 square feet. The facility will incorporate next-generation warehouse technologies designed to increase storage capacity and accelerate order picking. The project highlights how rising throughput requirements are supporting investment in larger and more automated distribution facilities.

5) Cold chain demand is benefiting from rising fresh food consumption and pharmaceutical reshoring

Cold chain storage demand is becoming a stronger driver of warehouse construction as fresh food distribution and pharmaceutical logistics require more specialized infrastructure. Coca-Cola Beverages Northeast is replacing an older facility with a new repackaging and distribution site in Halfmoon, including warehouse space and cooler services. In healthcare, Cardinal Health and Cencora are investing in highly automated pharmaceutical distribution facilities, with Cencora also expanding refrigerated and frozen capacity to support specialty medicines. BJ’s, Dollar Tree, and Chick-fil-A are also expanding distribution capacity to support grocery, foodservice, and regional store replenishment. Together, these projects show how rising demand for fresh food, temperature-controlled logistics, and resilient pharmaceutical supply chains is supporting a new wave of cold chain-related warehouse investment.

6) Automotive spare parts distribution is increasingly focused on faster fulfilment

Automotive spare parts distribution is increasingly focused on faster fulfillment as OEMs seek to improve service levels and reduce downtime for customers. Reflecting this trend, Stellantis is expanding its network with a new automated parts distribution center in Georgia featuring an AutoStore system to improve order speed and inventory accuracy. Similarly, Volvo Group is investing $37.7 million in a new regional distribution center in Tacoma, Washington, designed to reduce delivery times by up to two days and support more than 240 dealers across the Northwestern U.S. and Western Canada. These projects highlight how automotive manufacturers are investing in more responsive and automated spare parts networks to improve availability and accelerate deliveries.

Final thought: The Next Wave Is Taking Shape, But Nothing Is Set in Stone

The growing pipeline of projects scheduled for completion in 2027 suggests that the next expansion cycle in U.S. warehouse construction is already taking shape. Importantly, many of these facilities are the result of projects that have been in planning or development for the last two years, reflecting a backlog of investment decisions made during a period marked by supply chain disruptions, inflation, and elevated construction costs. As these delayed projects finally move forward, activity is set to accelerate. However, the outlook remains highly dependent on the external environment. Additional geopolitical shocks, renewed supply chain disruptions, or a deterioration in economic conditions could once again delay projects and push investment further into the future. While the direction of travel points toward stronger warehouse construction activity, the timing of that recovery remains vulnerable to another round of unexpected disruptions.

Discover the Warehouse Building Stock Database:

|

How can our research help you?

Want to explore the data behind these trends? The projects highlighted in this article represent only a small sample of the thousands of warehouse developments tracked by Interact Analysis. Our Warehouse Building Stock Database provides detailed forecasts of warehouse construction activity, building stock, end markets, and automation opportunities through 2030, helping suppliers identify where the next wave of logistics investment is emerging. To learn more about our market intelligence, contact us today

About the Author

Senior Analyst Matthieu Kulezak