- The humanoid robot sector is ‘an emerging market with huge opportunities for growth’.

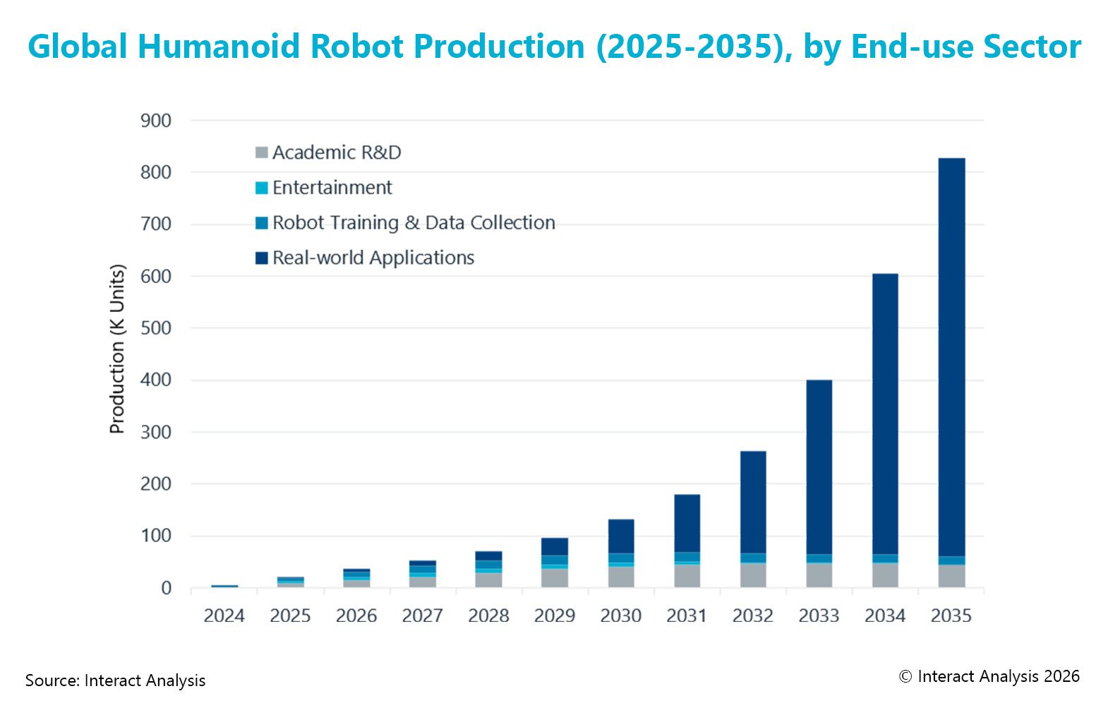

- Annual shipments projected to reach >700,000 units and $15bn revenue by 2035.

- China is expected to account for over 65% of real-world application shipments in 2035.

- Only ~10% of the robots produced were deployed in real-world operations by 2025, but this segment will become dominant by 2035.

Humanoid robots are not yet seeing commercial deployment at scale in the workforce, but strong growth is forecast during the 2030s. According to new research from Interact Analysis, with annual shipments still below 100,000 units, demand is driven by small-scale deployments, subsidies, and strategic partnerships rather than workforce-scale commercial economics.

The new Humanoid Robots – 2026 report from the market intelligence specialist predicts that the long-term commercial inflection point will occur in 2032, with shipments exceeding 700,000 units in 2035 and market revenue reaching approximately $15 billion. However, this outlook remains conditional on achieving economic viability thresholds, as well as breakthroughs in embodied AI to enable autonomous, reliable task execution, clearer regulatory frameworks, and acceptable efficiency rates.

China and the US to dominate humanoid robot demand by 2035

By 2035, Interact Analysis anticipates China will account for over 65% of real-world application shipments. This will be driven by government investment, subsidies, and procurement by state-owned enterprises. The US market, in a distant second place, will see growth driven by capital markets, AI investment, and high labor costs. Together, China and the US will account for over 85% of the demand for humanoid robots by 2035.

Short-term mass commercialization of humanoid robots is restricted by immature core technologies and the lack of established regulations and industry standards. At present, industrial manufacturing and warehousing are leading near-term deployments due to structured environments and a high concentration of early technology adopters. This is followed by public services, driven by Chinese state-backed programs. Household use cases remain a longer-term opportunity, constrained by safety and environmental complexity.

Four end-use sectors forecast to experience transformative growth

Interact Analysis forecasts that the following four end-use sectors will show significant growth in humanoid robot adoption through 2035:

- Real-world applications

- Academic R&D

- Robot training and data collection

- Entertainment

While academic R&D and entertainment applications currently dominate production volume statistics, both are expected to grow at more moderate rates once markets mature. The robot training and data collection sector, on the other hand, is forecast to expand in the short term but stabilize over the long term as simulation technologies advance. However, the most transformative growth is expected to come from the real-world applications sector, which is forecast to expand from around 10% of total production in 2025 to become the dominant market segment by 2035.

|

Marco Wang, Research Analyst at Interact Analysis, says, “Within the humanoid robots market, technology readiness remains a primary constraint, with gaps in embodied AI capability, severe data scarcity, and insufficient hardware durability and manufacturing consistency. Ecosystem and risk frameworks remain underdeveloped, with safety standards, certification pathways, and insurance mechanisms still required to enable economically viable deployment.