Humanoid robot production witnessed significant growth in 2025. However, growth was highly concentrated in China and masks a significant deployment gap. Our latest report, Humanoid Robots – 2026, reveals autonomous and commercially viable real-world deployments remains limited.

A 10x leap in production, yet real-world use increases by just 10%

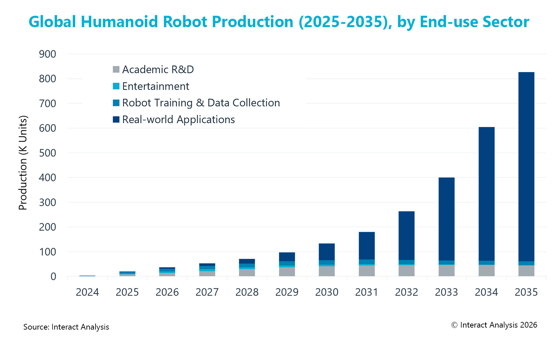

Global humanoid robot production exceeded 20,000 units in 2025, a tenfold increase from fewer than 2,000 units in 2024. However, the vast majority were used for research, data collection, and entertainment. Only around 10% of units produced were deployed in real-world applications. While this represents a substantial increase from dozens of units in 2024, growth was driven more by an expanding customer base and increasingly diversified pilots than by scaled commercial deployments.

By the end of 2025, most real-world application projects remained small-scale proof-of-concept (POC) deployments, predominantly driven by government subsidies, strategic investments, and supply chain partnerships. The market still lacks large-scale, long-term deployments based purely on commercial rationale. Although cost reduction and efficiency improvements through automation may have been the original intent of many pilot projects, most had not progressed beyond short-term demonstrations and small-scale controlled operations.

Autonomous operation, return on investment realization (requiring sufficient efficiency and task success rates), and multi-task-level generalization capabilities still appear to form the “impossible triangle” that humanoid robots struggle to break through.

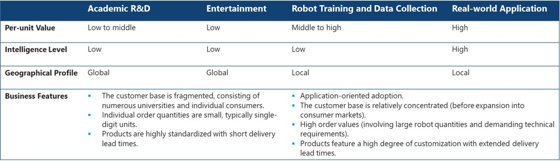

|

Chinese vendors lead humanoid robots production

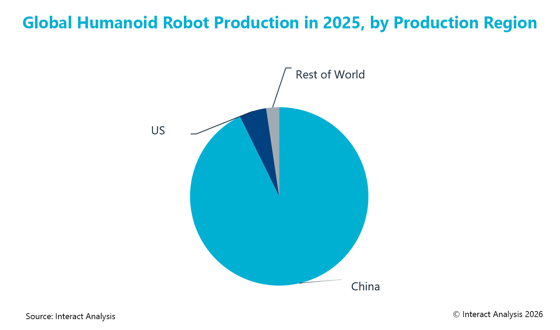

China was the engine of both supply and the early adoption of humanoid robots during 2025. In terms of overall unit production, Chinese vendors’ share exceeds 90%, with the remainder largely from US manufacturers. In terms of adoptions, about 75% of humanoid robots were delivered in China. The disparity between domestic production and demand in China during 2025 is primarily due to significant overseas sales achieved by several Chinese humanoid robot manufacturers, with demand driven mainly by academic research and entertainment use.

|

To learn more about our report, download a brochure.

The vendor landscape is also highly concentrated in China. The top 5 producers in 2025 were all Chinese manufacturers, collectively accounting for approximately 70% of global humanoid robot production. Unitree and Agibot each produced and shipped over 5,000 units, together surpassing 11,000 units and representing more than 50% of the global market.

However, today’s market concentration and leadership are driven by early research demand (including data collection for physical AI training), attempts to gain media attention, and curiosity-driven trials, rather than by proven commercial deployments. The robust material support provided by the Chinese government for humanoid robotics is the primary reason behind the aggressive expansion of Chinese vendors and the domestic market in 2025. We believe the competitive landscape is far from settled, given that both the market and the underlying technology remain in a very nascent, immature phase. It could still experience substantial dynamical change, with more established cross-industry players joining the field, such as leading automotive and consumer electronics vendors.

More than 5 years to reach large-scale commercial inflection point

Looking ahead, we believe the market is likely to continue growing, with annual volumes reaching thousands of units. The share of units deployed for real-world applications will increase gradually over time. However, in the short run, growth won’t be entirely driven by rational commercial considerations. It is primarily driven by numerous small-scale pilots at present, rather than large-scale commercial projects. Customers will be concentrated among well-capitalized companies and enterprises with capital and supply chain ties to humanoid robot companies, and government involvement will play a key role.

We believe that near-term deployments will remain predominantly semi-autonomous, with certain specific tasks still requiring rule-based control or human teleoperation. The latter is expected to achieve the first actual commercial deployment of humanoid robots in hazardous work scenarios and regions with significant regional labor cost disparities. In contrast, highly autonomous, AI-driven humanoid robots will initially be adopted in scenarios with greater tolerance for task speed and error rates.

Our field observations indicate deploying humanoid robots at scale for tangible workforce value remains constrained by critical usability gaps (including task reliability and efficiency insufficient to achieve ROI, and limited multi-tasking capabilities). Technical bottlenecks span immature embodied AI, severe physical data scarcity, and inadequate hardware endurance. Meanwhile, the absence of established safety standards and regulatory frameworks constitutes a key barrier to expanding humanoid robots into human-machine interactive settings.

Consequently, we expect the market will struggle to achieve a large-scale commercial inflection point across multiple domains within the next five years. A commercial inflection point is forecast post-2032, contingent on breakthroughs in autonomous and reliable task execution, acceptable ROI, and clearer regulatory environments. By 2035, global shipments for real-world applications are projected to exceed 700,000 units, with market revenue reaching approximately $15 billion.

|