While manufacturers continue to navigate higher equipment costs and shifting trade policies, the outlook for the material handling industry is increasingly encouraging.

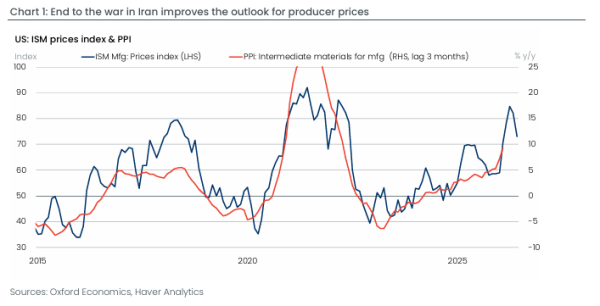

One of the biggest positive developments this month is the easing of geopolitical tensions in the Middle East, which has helped lower fuel prices and improve confidence across the manufacturing sector. Although steel, aluminum, and other raw material costs remain elevated, overall price pressures appear to be stabilizing.

Manufacturing activity continues to expand, particularly in industries such as defense, semiconductor production, and advanced manufacturing. These sectors are investing in new facilities, automation, and warehouse operations—all of which support continued demand for forklifts, warehouse equipment, and material handling solutions.

Supply chains are also showing signs of improvement. Shorter supplier lead times and increasing inventory levels should help improve equipment availability and reduce delays for customers planning fleet additions or replacements.

At the same time, many businesses are choosing to extend the life of their current equipment rather than make immediate capital investments. That trend continues to drive demand for planned maintenance, replacement parts, repairs, and rental equipment to keep operations running efficiently.

What This Means for Your Business

- Equipment pricing is beginning to stabilize, although steel, aluminum, and tariffs continue to influence costs.

- Manufacturing growth remains strong across several key industries, supporting future demand for material-handling equipment.

- Supply chain improvements are helping shorten lead times and improve equipment availability.

- Service, maintenance, rentals, and fleet optimization remain cost-effective strategies for maximizing uptime while managing capital expenses.

The July 2026 newsletter from Oxford Economics reported that the ISM manufacturing index fell by 0.7 pp to 53.3 in June, in line with our expectations. The report details point to a positive outlook for the sector. The supplier deliveries index registered the largest drag on the headline index, falling by 3.2pp, indicating an improvement in supply conditions. New orders and production fell modestly in June but remain well within expansion territory. Defense and semiconductor-related machinery demand were the brightest spots, and we expect these sectors to drive growth amid supportive fiscal policy and a seemingly insatiable AI buildout. Inventories moved into expansion territory for the first time since April 2025. With customer inventories still in “too low” territory, the inventory upswing will likely gain momentum.