For nearly 40 years, Wells Fargo Equipment Finance and its predecessors have surveyed construction industry executives annually to better understand the unique challenges that decision-makers face. Over the last five years, we’ve seen slow but steady growth that has made this industry more and more appealing. The results of our 2015 survey of construction industry executives revealed a sense of optimism that has held up well through the first three quarters of this year. Two themes we saw play out in 2015 were that equipment rentals would remain strong and equipment acquisitions would likely rise, although at a pace that most industry participants would like to see more accelerated than is currently taking place.

As the fourth quarter comes to a close there are two key legislative items that are important to companies in this space that could invigorate the industry if resolved in a timely manner. A highway funding bill and reinstatement of bonus depreciation could have a positive impact for manufacturers, distributors, rental companies and equipment end users. Banks and independent finance companies that rely on this industry to deploy longer term capital would also benefit. How much of a benefit is open to interpretation.

Industry Environment Residential and Non-residential Spending

Residential spending has been slowly increasing as noted by the latest report from our Wells Fargo economists. The report noted that private multifamily spending jumped 4.8%, while single-family spending increased a more modest 0.7%. This was not terribly surprising following the weak housing starts number in August.

Non-residential construction activity is increasing. Most areas of the country are seeing a rise in non-energy related commercial and infrastructure spending. A look at the number of projects valued at over $5 million that are either in the planning, bidding or post-bid stage shows a year-over-year increase of 30% from October 2014 to October 2015. The states with the highest percentage increases are Kentucky (83%), Oklahoma (75%), Wisconsin (73%), Massachusetts (73%) and Utah (71%). Only one state, Montana, is showing a decline in large project activity at -21%. The next lowest state for growth is Tennessee at a positive 24%.

The positive, even if modest, growth numbers for both residential and non-residential construction are good indicators that this industry can remain healthy going into 2016, though with some notes of caution, particularly the continuing impact of the slowdown in the energy sector.

Oil and Gas

The recent slowdown in oil and gas drilling, resulting from the high supply and low demand environment, which in turn drove down the price of oil, has impacted the utilization of both Original Equipment Manufacturer (OEM) dealer rental and general rental fleets. According to industry sources, the overall rig count in the U.S. is down 59% from October 2014 to October 2015. The reduced activity surrounding new well activity has impacted distributors, contractors and rental companies in areas with a higher concentration of energy production. The positive news in these areas is that as equipment comes off of production jobs in energy, it has been absorbed into other construction related activities. The downside to this is that there has been recent pressure on pricing for non-energy related projects as well as downward pressure on rental rates and used equipment rates for assets related to the energy industry. It is yet to be determined what the long term impact of this protracted slow-down will be on the overall construction industry, but as of today, there appears to be sufficient activity on a national basis to absorb the loss of energy related activity in the industry.

Continued Acceleration in Rental Activity

Rental industry information contributed by Gary Dyshaw, Wells Fargo Bank’s Heavy Equipment Dealer Group and Gary McArdle of Rouse Rental Services.

The growth in heavy equipment dealer and rental house balance sheets during the last two to three years has been driven, in part, by organic growth, but also by changes in market conditions which have spawned significant increases in rental fleet portfolios. These changes include:

- Unpredictable work backlogs and projected business activity levels, which in turn, have contributed to unwillingness by contractors to commit to equipment purchases. Lack of an extended Federal infrastructure funding bill has added to this uncertainty.

- A number of end-users whose financial conditions remain weakened by the economic downturn, and therefore are having to rely on rental arrangements (rather than purchases) to obtain equipment they need for their business.

- Demand from bonding companies to shift debt/liabilities off contractor balance sheets.

- End-users in the oil/gas industries for which short-term rental contracts better align with their market volatility.

- Broader OEM support for increased rental activity in their dealer network.

Sentiment in the rental sector over the first half of 2015 has been a mixture of optimism and concern. Most of the economic data and construction spending estimates point toward high single digit growth in non-residential construction spending for the next few years. This should be a positive signal for OEM dealer rental distributors as well as general rental houses which have seen dramatic growth over the last four years even while construction spending improved only slightly.

Rental houses and dealers have had to increase rental inventory fleets to accommodate this increased rental activity. Rental rates are up 25.5% since January of 2011 according to the April Rouse Rate Index. Used equipment prices have weakened in the first half of 2015, but still remain 7.1% higher than the prior peak period of April 2007 and 56% higher than the trough period in June 2009, according to the June Rouse Value Index.

Many dealers believe that when a Federal Highway bill is passed and the economic outlook stabilizes, contractors would rather own than rent their core equipment and will return to the market. Others feel that this will be a permanent shift to renting equipment rather than owning.

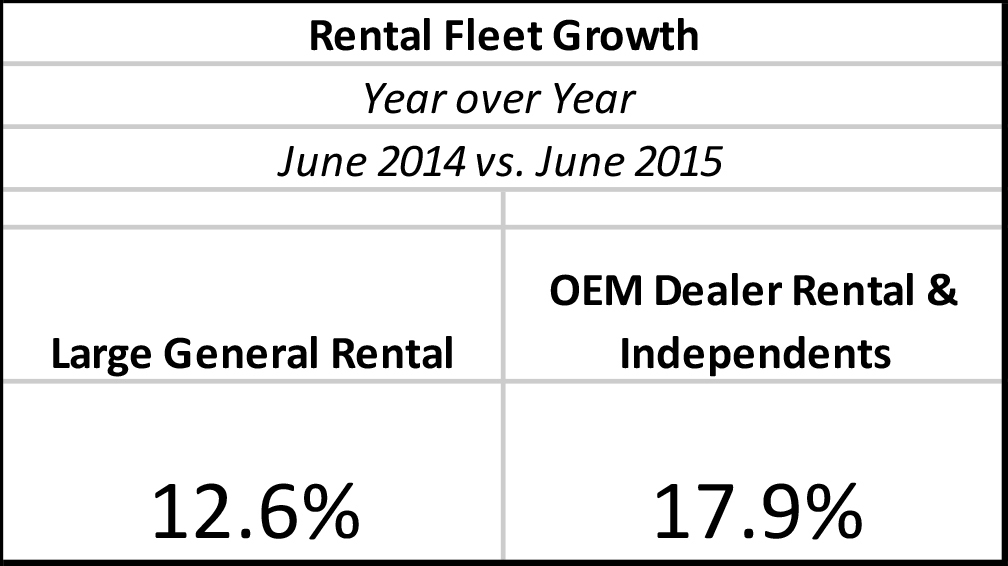

Rental Fleet Size

Rental fleet sizes have increased dramatically since 2010 in order to meet increasing rental demand. The fleet sizes of the major national and regional rental companies have increased over 55% on an original equipment cost (OEC) basis since 2010. In just the last year (from June 2014 to June 2015), the large general rental companies have increased their fleet OEC by 12.6% and the OEM dealer rental and independents have increased their rental fleet size by 17.9% (see Exhibit 1).

Exhibit 1

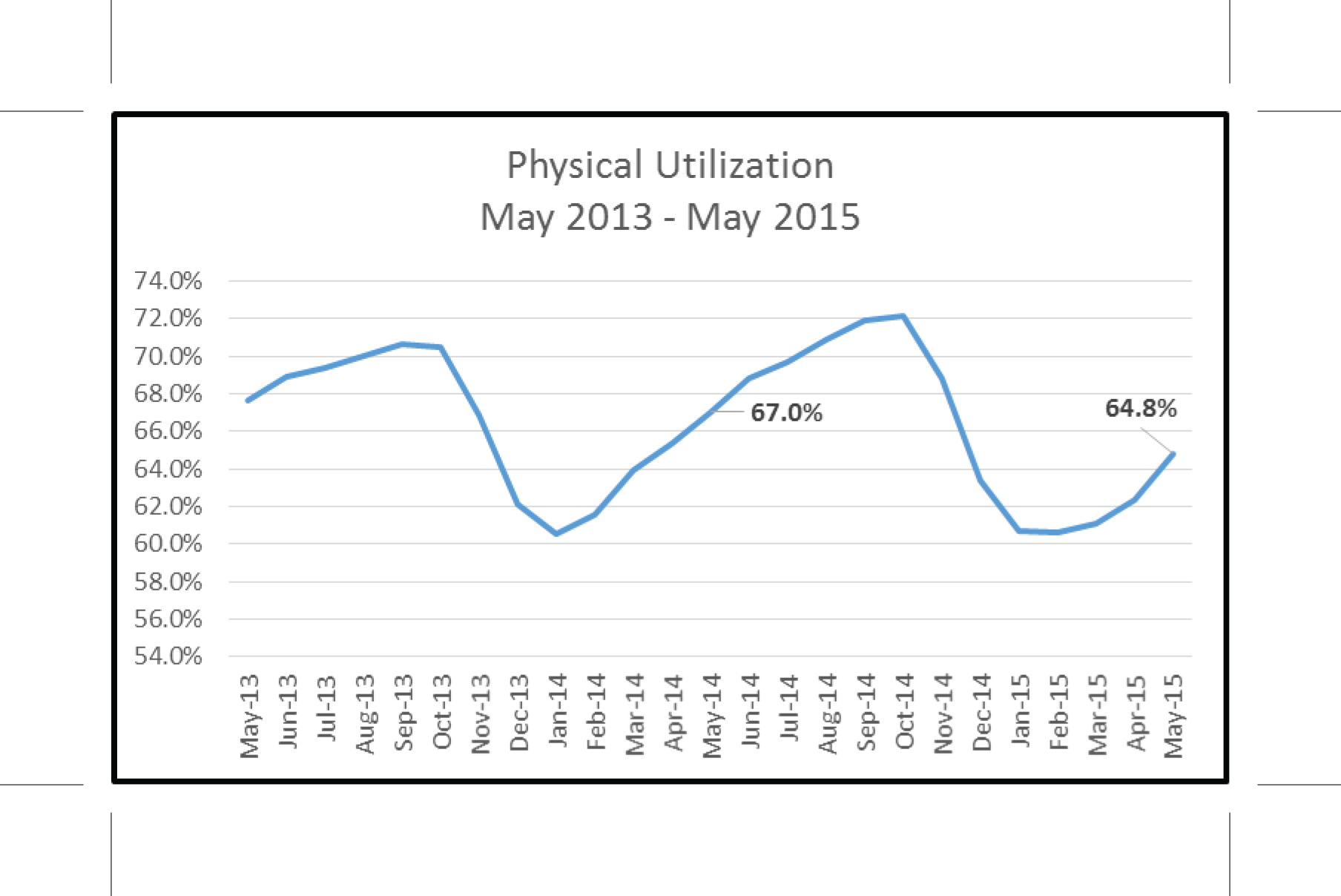

Utilization

Utilization (Avg. OEC on rent / Avg. OEC) has been coming in lower on a year over year basis beginning in February 2015, peaking at 3.3% down year over year in April and improving to 2.2% down in May 2015. Most of this lower utilization is a result of lower demand and utilization in the oil and gas end markets as well as weather effects that extended into May this year (see Exhibit 2).

Exhibit 2

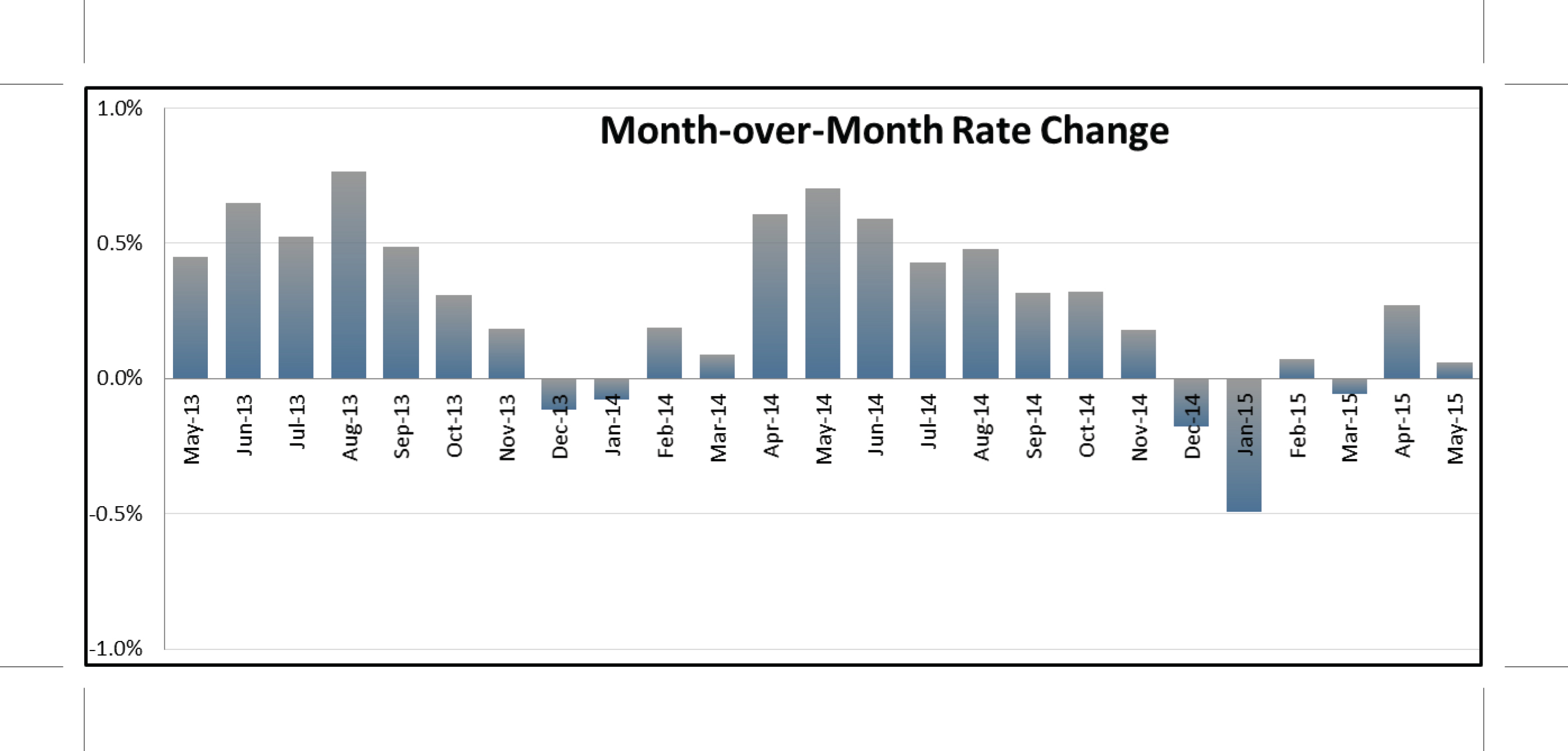

Rental Rates

Rental rates, which have seen a nearly 26% increase since January 2011, came under pressure in the first half of 2015 for much of the industry. While most OEM dealers and general rental companies continue to see higher average equipment costs, many have had a more difficult time in the first half of 2015 passing on these higher costs to customers in the form of higher rental rates. On average, rates went down slightly in March this year, which was the first rate decline observed by Rouse for a month other than December or January since 2011. April and May rates improve slightly on a sequential basis (see Exhibit 3).

Exhibit 3

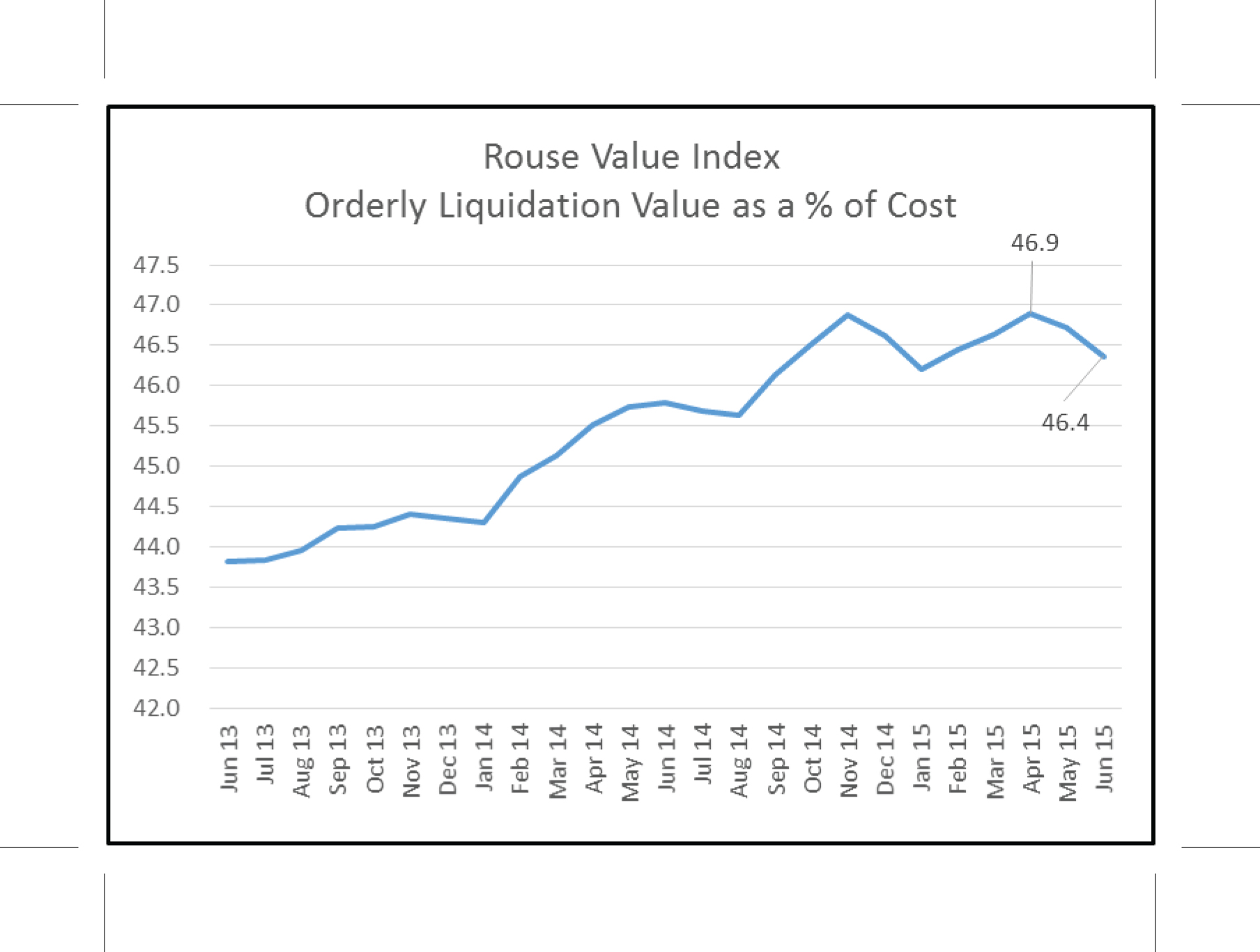

Equipment Values

Equipment values have improved dramatically since April 2009 (the low point of the previous economic downturn) and, based on the Rouse Value Index, are currently running 56.2% higher than the trough. Lower auction prices in the second quarter of 2015, largely attributed to the stronger dollar having an impact on foreign purchasing power, have begun to impact the index, which in June came in at 0.8% below the May index value (see Exhibit 4).

Exhibit 4

Equipment Acquisition Preferences

There is no doubt that there is an increased trend toward renting equipment in the industry, but that does not mean that purchasing equipment has disappeared. End users still acquire equipment for their business on a regular basis and will continue to do so. What has happened is the typical end user of construction related equipment has become more sophisticated in their fleet management planning than in decades past. In addition, manufacturers, dealers and rental companies have deployed their own capital in the form of dedicated rental fleets to expand the choices and options of which their end users can take advantage.

Contractors who may have typically purchased a specific amount of equipment of a certain type on a yearly basis can now take a more conservative approach to their planning needs. They are confident that if they are short two backhoes and two wheel loaders for a specific project, they will be able to obtain the use of the assets they need on almost a moment’s notice. This gives them the ability to wait for just the right deal or the guaranteed certainty of long term work to make the purchase decision. This gives the user significant leverage in the purchasing process as the prospect of lack of availability is absent from the equation. Contractors can instead focus on their overall economic situation when deciding whether or not to buy an asset.

Conclusion

Buying patterns and attitudes towards ownership of construction equipment continue to evolve in this industry. Ownership still makes good economic sense for many contractors but the availability of good quality rental equipment at competitive rental rates gives them attractive options. The increased cost of the additional availability of rental equipment is shifting the burden of leverage away from the contractor, the end user of the equipment, to the companies that are providing the rental fleets — namely manufacturers, dealers and rental companies. This has caused the expansion of their balance sheets in order to pay for the increase in their fleets. These companies have been helped significantly by the historically low interest rates that we have enjoyed over the past several years. How long the rates will continue to be low remains to be seen and is one area that the industry should be cognizant of when evaluating our current and future environments.

If conditions do change, and owning large rental fleets becomes more burdensome, this could lead to a shortage in availability of rental equipment. Contractors could be forced to re-evaluate their usage and acquisition practices.

Overall, construction continues to be a strong business for Wells Fargo and we remain positive on residential and commercial construction activity. We see significant opportunities for equipment financing and leasing as we look toward 2016.

Wells Fargo Equipment Finance will be concluding its annual Construction Industry Forecast in November. The results will be published in mid-January and will allow us to continue to provide timely and accurate insight into the trends expected by key industry executives in the construction equipment industry.