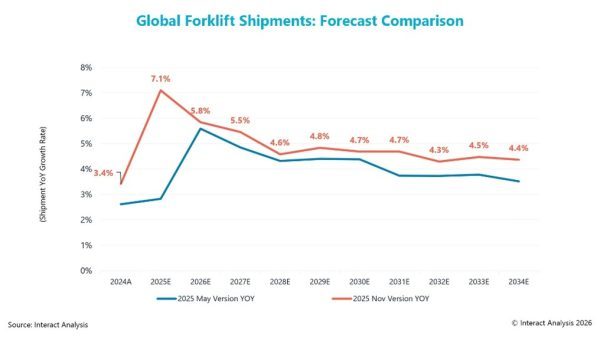

The global forklift market is entering a period of renewed momentum, with updated forecasts indicating stronger growth in the near term and over the next decade. According to the latest research from Interact Analysis, shipment growth reached 7.1% year-on-year in 2025, a notable jump from 3.4% in 2024. More importantly for dealers, this acceleration is not expected to be a short-term spike. Instead, analysts are now forecasting a robust average annual growth rate of 5% from 2024 through 2034, reflecting what they describe as a “sustained structural improvement” in the market.

The Interact Analysis market report focuses on Class 1–5 forklifts used primarily in manufacturing and logistics environments, providing detailed insights into accelerating trends in electrification and autonomy that are reshaping customer buying behavior and fleet strategies.

For forklift dealers, this revised outlook signals expanding opportunities across new equipment sales, fleet replacement programs, electrification projects, automation, and aftermarket services.

Annual Orders Set to Exceed 3.6 Million Units

Interact Analysis has upgraded its long-term forecast, now projecting global annual forklift orders to exceed 3.6 million units by 2034—an increase of 400,000 units compared with earlier expectations. This scale of growth underscores a steadily expanding installed base, with direct implications for parts, service, operator training, and fleet management offerings.

Dealers positioned to support long-term customer relationships—rather than one-off equipment transactions—are likely to benefit most as fleets grow larger, become more technologically advanced, and increasingly adopt electric units.

China and India Drive Global Demand

Nearly 80% of projected global growth over the next decade is expected to come from China and India, with China alone accounting for more than 70% of the anticipated increase in unit demand. Forecasts suggest China’s contribution will continue to widen, particularly between 2030 and 2034.

While this growth is concentrated in Asia, its effects will be felt globally. Higher production volumes, faster technology cycles, and rising competition among manufacturers are likely to influence pricing, availability, and feature expectations in other regions—particularly around electric Class 1–3 trucks and automation-ready platforms.

End Customers Signal Increased Investment

One of the most encouraging indicators for dealers is growing optimism among end users. Interact Analysis reports that 50% of surveyed customers expect to increase their investment in material handling equipment by more than 10% in 2026. This confidence is largely driven by accelerating automation in manufacturing and logistics, alongside rising labor costs and persistent workforce shortages.

At the same time, many automation equipment manufacturers remain cautious due to macroeconomic volatility, geopolitical uncertainty, supply chain disruptions, and component availability challenges. For dealers, this gap between demand and supply-side caution creates opportunities to provide flexible solutions and phased automation strategies.

Electrification, Automation, and Fleet Replacement

Maya Xiao, APAC Research Manager at Interact Analysis, identifies several key drivers shaping the market’s long-term trajectory. Rising demand for automation is fueling investment in advanced material handling solutions, while the dual shift toward electrification and autonomy is accelerating fleet replacement cycles.

For dealers, these trends translate into more frequent conversations around the total cost of ownership, charging infrastructure, battery technology, software integration, and operator training—areas where consultative selling and value-added services can differentiate offerings.

Emerging Markets and Long-Term Labor Pressures

Beyond China and India, emerging markets in Southeast Asia, the Middle East, and Africa are adding further growth momentum, supported by infrastructure investment and supply chain reorganization. Meanwhile, ageing populations, rising wages, and ongoing recruitment challenges are making automation a strategic necessity rather than an optional upgrade.

Together, these forces create a favorable environment for the forklift industry over the next decade. For dealers, the upgraded 5% annual growth forecast underscores the importance of aligning portfolios and capabilities with electrification, autonomy, and long-term customer support, positioning them not just as equipment suppliers but as partners in productivity and workforce transformation.

About the Author:

With over 200 years of combined experience, Interact Analysis is the market intelligence authority for global supply chain automation. Their research covers the entire automation value chain – from the technology used to automate factory production, through inventory storage and distribution channels, to the transportation of the finished goods. www.InteractAnalysis.com